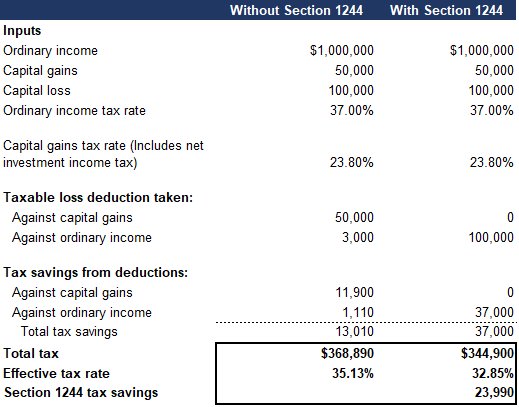

Generally, capital losses can only be taken against capital gains with a limit of $3k annually against ordinary income. There is a material tax difference between allowing the losses against ordinary income vs. capital gains due to the tax rates. Below is an example with and without Section 1244:

The tax savings for this taxpayer are $23,900 with a drop in the effective tax rate of 2.28% due to the Section 1244 election. The tax savings will be different for every taxpayer but this is a snapshot of the potential tax savings Section 1244 can unlock.

This article does not constitute legal or tax advice. Please consult with your legal or tax advisor with respect to your particular circumstance.