Qualified Small Business Stock (QSBS) Facts:

- Up to a 100% capital gains exclusion (i.e. a 23.8%+ increase in returns!)

- Boosting “after-tax” gains = more attractive investment

- QSBS is only one of many tax incentives that could benefit your company

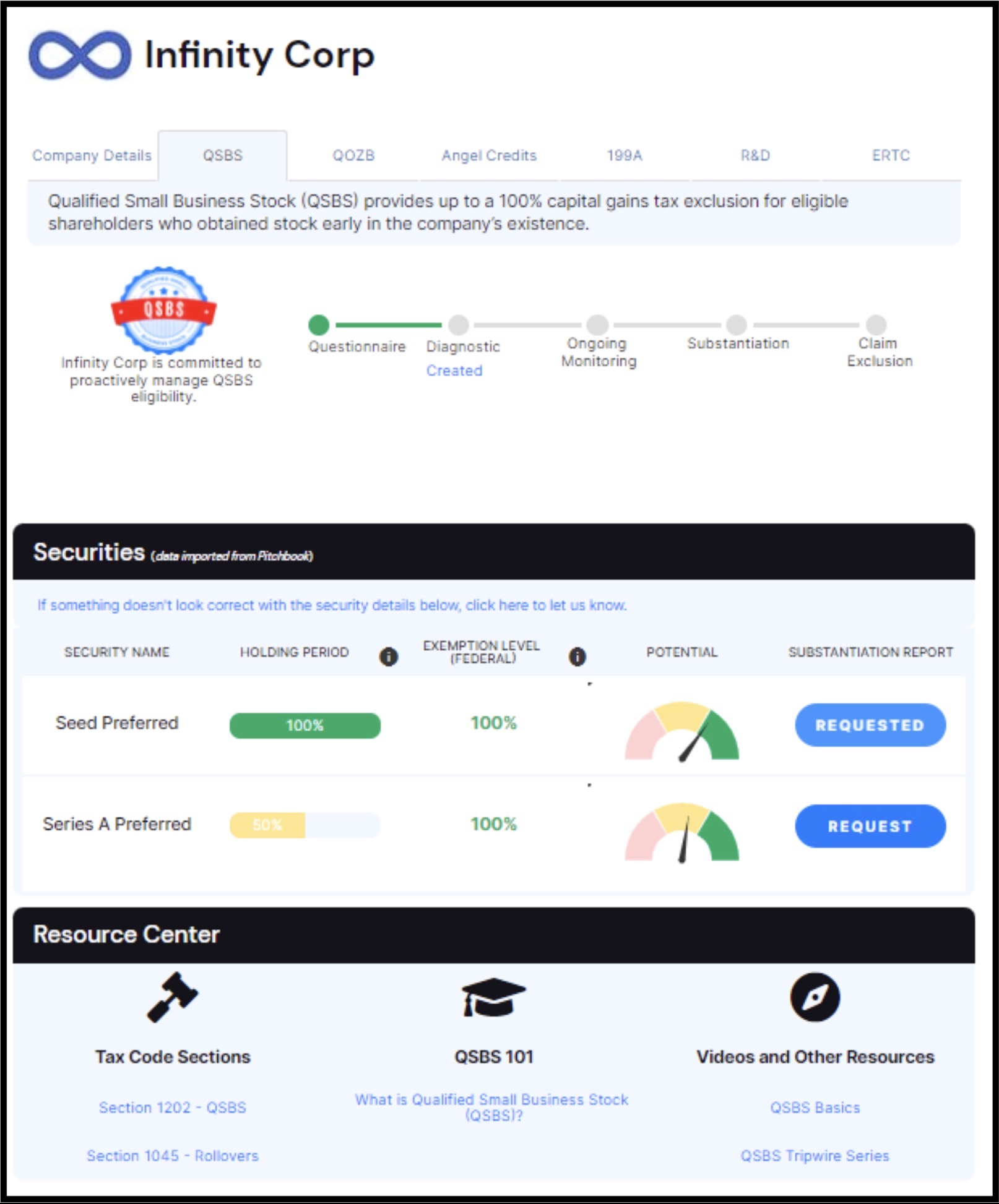

Complete the questionnaire

10 questions – should take 5 minutes

View your QSBS profile and address any follow-up questions

Monitor your securities and stay up to date regarding relevant developments

5 keys to qualify for the QSBS tax exemption

Don’t just take our word for the benefits of QSBS, hear investor Jay Kapoor explain the ABCs of QSBS.

Stock has to have been issued after August 10, 1993 to be QSBS eligible, and may be eligible for either a 50%, 75%, or 100% capital gains tax exclusion depending on when the stock was issued.

To qualify for the QSBS exclusion, stock needs to have been held for at least 5 years. The holding period start date varies based on security type (i.e. for stock options the holding period starts when the options are exercised as opposed to when they were granted).

If stock is sold before the 5-year mark, it may be eligible to be rolled over into other QSBS stock and continue to count towards the 5-year period, pursuant to IRC Section 1045.

At the time stock is issued, the company must be a domestic US C-Corporation with less than $50M in “gross assets” (i.e. tax basis of assets).

Active Business Requirements entail that the company primarily utilized its assets for qualified purposes. This is demonstrated through various tests.

The Company must not have repurchased a “significant” amount of stock during the period one year before and one year after issuance. Particular shareholders (or related parties) looking to claim the exclusion must not have had their stock repurchased by the company within 2 years of when their stock was issued.

Top 10 Founder Questions

QSBS (Internal Revenue Code Section 1202) was created in 1993 to spur economic development. Recognizing that early-stage companies account for the majority of new job creation, legislators sought to “level the playing field” by providing entrepreneurs and those that join and invest in them tax-advantaged equity.

The QSBS benefit was expanded to up to 100% capital gains tax savings in 2010.

As stated by President Barack Obama,

“One of the great things about America is that we are a nation of doers — not just talkers, but doers. We think big. We take risks. And we believe that anyone with a solid plan and a willingness to work hard can turn even the most improbable idea into a successful business…This is a country that’s always been on the cutting edge. And the reason is that America has always had the most daring entrepreneurs in the world.”

– President Obama, JOBS Act signing, April 5, 2012

Eligible shareholders can save up to 100% of capital gains taxes on the sale of QSBS held for at least 5-years. Gains available for the exclusion are limited to the greater of $10 million or 10x the taxpayer’s basis.

Companies realize several benefits from being a “Qualified Small Business”, such as:

- Making their equity more attractive to investors.

- Avoiding negative investor sentiment if/when investors expect their stock to be QSBS eligible.

- Potentially attracting investors looking to roll their gains from other QSBS stock held less than 5 years into another Qualified Small Business. Rolling QSBS gains (per IRC Section 1045) enable a taxpayer to continue working towards their 5-year holding period to ultimately benefit from tax-free gains, however rollovers need to be made within 60 days of the realized gain.

Corporate level Qualified Small Business stock requirements include that the Company:

- Is a domestic US C-Corporation with less than $50 million in Aggregate Gross Assets when the stock is issued.

- Utilized its assets towards a qualified trade or business during “substantially all” of the shareholder’s holding period (i.e. the Active Business requirements),

- Did not undertake disqualifying stock redemptions (i.e. stock buy-backs) within a year of the QSBS stock being issued.

The best way to ensure your company is eligible to issue QSBS stock is to perform an analysis of your company against the criteria. QSBS Expert (CapGains Inc.) offers two main approaches, which generally depend on your company’s stage:

- QSBS Representation Validation (risk analysis): $4,500 one-time fee

Provides a risk-based approach to monitor and proactively manage a corporation’s potential eligibility to issue QSBS stock. This is most applicable early on in a company’s life cycle and in preparation for a financing round. - Comprehensive Company Level QSBS Analysis: $2,500 per year analyzed

Historical assessment of a company’s potential eligibility. Analysis provides an overall timeline of when a company appears to have met the QSBS eligibility criteria. This is most applicable at the time of a corporate exit and/or if certain shareholders are able to sell their shares.

Get started today by seeing how your company stacks up against the general QSBS criteria by taking our free eligibility quiz.

IRC Section 1202(d)(1)(C) states that if/when the IRS requires companies to report a QSBA analysis, “such corporation agrees to submit such reports to the Secretary and to shareholders as the Secretary may require to carry out the purposes of this section.”

There are many situations that may jeopardize a company’s QSBS eligibility, but highlighted below are a few of the most common eligibility tripwires:

- Being taxed as other than a C-corp – When stock is issued the company must be taxed as a C-corp to qualify. Many companies make S-elections or are established first as LLCs taxed as partnerships. SwagUp CEO shares how his QSBS ignorance cost him $75M

- Material foreign operations – QSBS was designed to incentivize economic activity in the United States. Material foreign operations need to be assessed for the potential impact on various eligibility criteria.

- Significant Stock Redemptions – Often after a company completes a large financing round they provide liquidity to founders or early employees through repurchasing a portion of their stock. While these redemptions are likely well deserved, they can jeopardize the eligibility of the stock that had just been issued.

In addition to the corporate level requirements, certain shareholder level requirements need to have been met in order to benefit from the QSBS tax exclusion, such as:

- Acquired by the taxpayer at its original issue.

- Held for at least 5 years before its sale or exchange.

- Been held by an eligible holder (i.e. individual).

With specific security types, the start of the holding period generally depends on when the securities became actual stock; for example:

- Stock options – holding period generally starts when the options are exercised rather than when granted (provided the corporate level requirements are met when the options are exercised).

- Restricted Stock Awards – holding period generally begins if/when an 83(b) election is filed.

- Convertible notes – holding period generally start once the notes convert to stock.

- Simple Agreements for Equity or “SAFEs” – the holding period for SAFEs is a QSBS “gray area”. Certain SAFEs include terms that may make them more akin to equity securities and therefore more likely to be QSBS eligible when issued, however these need to be looked at on a case by case basis.

Often investors tell us they never want to invest in another company that is not QSBS eligible. After all, if you have two similar performing companies and one returns ~25% more to you, it is hard to argue that you’d feel differently if you were an investor.

The good news is that with a little planning you can leverage this potential tax savings for your investors to your advantage as you approach your fundraising efforts. Validating eligibility and making potential investors aware of it can increase the likelihood of acquiring fundraising as well as the confidence investors have in your company.

Additionally, if an investor in another company realizes a QSBS gain in under the required 5-year holding period, they can roll their gain into another QSBS stock and only have 60 days to do it…in other words there are investors looking for eligible QSBS stock just like yours right now and are incentivized to invest!

If shareholders have realized a gain before the 5-year holding period is met, the Section 1045 rollover allows for the reinvesting of QSBS sale proceeds into one or more newly issued QSB stocks. To qualify for the 1045 rollover, one must reinvest their proceeds within 60 days from realizing their gains.

Learn more about the section 1045 rollover here:

During early financing rounds (i.e. Series Seed Preferred, A, B, etc.) it has become standard practice for investors to request the company make representations regarding QSBS eligibility within the Share Purchase Agreement and include a corresponding covenant in the Investor’s Rights Agreement stating that the company will not take actions that could jeopardize the stock from qualifying as QSBS.

Without a deep knowledge of the QSBS requirements, corporations may not have a good handle on whether their company actually appears to meet the eligibility requirements and/or what actions could jeopardize eligibility going forward. Our QSBS Rep Validation analysis is meant to do just that as well as helping companies understand the rep and covenant and any non-standard changes or edits requested to these clauses.

QSBS and Early Stage Investing go hand in hand as investors can leverage QSBS for tax-free gains.

- QSBS eligibility aligns nicely with early stage companies as most of these companies have yet to reach the $50 million gross asset threshold.

- Investment funds and platforms also offer a unique opportunity to address one of the key hurdles with the QSBS rollover provision (for gains realized prior to the 5-year holding period) per Section 1045—namely that rollovers need to be made within 60 days of a gain.

Working with as many founders, investors and other stakeholders as we do, we come across many situations that have QSBS implications, so whether you are:

- Considering converting entity types to be eligible to benefit from QSBS

- Planning for an exit and looking to start a new company to roll your gains into

- Expecting that your gain will exceed the $10M QSBS exclusion limit

It is important to plan ahead to make sure actions are performed in ways that preserve QSBS for you and your shareholders. Feel free to write us at [email protected] and we can help you think through the matter or connect you to the right resource.