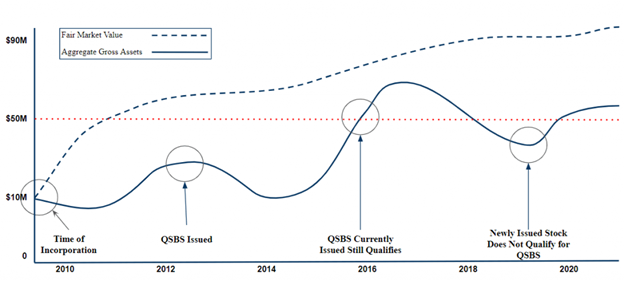

The QSBS “gross asset test” or “size test” requires that the aggregate gross asset value of the business must be below $50 million at all times before and immediately after the issuance of QSBS. If gross assets have ever exceeded $50 million, the business will not qualify to issue QSBS in the future, but QSBS issued before exceeding the threshold will still qualify, provided the other eligibility criteria are met.

As shown in the below timeline, it is ok for the corporation to exceed $50 million in gross assets during the required 5-year holding period after the QSBS is issued. However, additional securities issued at a later time would not qualify as QSBS if the Gross Assets exceeded $50mm at any point before issuance of those securities.

Aggregate gross assets include cash and the aggregate adjusted basis of other property held by the corporation. Section 1202(d)(2)

QSBS considers the tax basis of assets, which are generally reported on Schedule L of a corporation’s tax return (i.e. Form 1120). The value of assets would include intangible assets such as goodwill.

Basis is generally the amount of a company’s capital investment in property for tax purposes. Certain events may occur during the period of ownership which may increase or decrease basis, resulting in an “adjusted basis”. Basis can be increased by items such as the cost of improvements that add to the value of the property and can be decreased by items such as depreciation and insurance reimbursements for casualty and theft losses.

The QSBS regulations specify a couple of other common questions regarding “Aggregate Gross Assets”:

- The adjusted basis of any property contributed to the corporation is determined based on the fair market value at the time of the contribution.

- All subsidiaries controlled by the corporation (i.e. more than 50% owned) shall be aggregated and treated as one corporation for QSBS purposes.

- If the Corporation was converted from an LLC or other legal structure to a C Corporation the assets will have to be stepped up to FMV and there could be goodwill or intangibles reported, which may increase the basis of the assets on the balance sheet.

Business valuations are conducted on fair market value (FMV) basis, which means “the price at which property would change hands between a willing buyer and a willing seller, neither acting under compulsion to buy or to sell, both being able and willing to trade, both being well-informed about the property and the market for such property, and both having reasonable knowledge of relevant facts.” Sections 20.2031-1(b) and 25.2512-1

The gross asset test for section 1202 QSBS is conducted on an ‘aggregate gross assets’ basis, not fair market value.

Company valuations will not affect the gross asset test for QSBS purposes. Those valuations are based on how the investors value the business. However, the QSBS criteria are purely based on the asset side of the balance sheet (e.g. property or cash.)

For example, a startup is raising its Series B financing round at a pre-money valuation of $40 million and intends to raise $15 million (post-money valuation of $55 million). As long as the company does not have over $35 million in other assets on its balance sheet, the $15 million in cash received from the financing round will not cause the company to fail the gross asset test for QSBS purposes.

Investor documents such as Share Purchase Agreements may include a Qualified Small Business Stock clause, whereby the corporation indicates if their stock appears to qualify as QSBS before the stock is issued. For example, the clause may state the following regarding the gross asset test:

“aggregate gross assets, as defined by Section 1202(d)(2) of the Code, at no time between the date of its incorporation and the Closing, have exceeded U.S. $50 million, taking into account the assets of any corporations required to be aggregated with the Company in accordance with Section 1202(d)(3)of the Code.”

While these types of clauses are helpful support, the best sources of evidence for validating that the company passed the gross asset test include the company’s historical tax returns and its funding history. While the funding history is for the most part publicly available, the tax returns are likely unavailable to a minority shareholder. As an alternative, you may be able to leverage certain company reporting to help support your assertion that the company satisfies the Gross Asset test, however it is best to first see if the company will make such information available or request that they perform a Qualified Small Business assessment at the company level and share it with you.

At first glance, it might seem like the $50M Gross Asset Test is simple, but the reality is that in certain circumstances, it can be much more complex. For example, if a financing round has multiple closings, part of the stock issued during the round may qualify as QSBS, while some of it may not. Read more about this unique situation here.